Ever heard of the Home Owners Loan Act? If not, you’re not alone—but it changed mortgages forever. Here’s what banks won’t tell you.

1: Introduction – Myth Busted: The Home Owners Loan Act

“Just another dull old law, right? The Home Owners Loan Act was.”incorrect.

Most people believe the Home Owners Loan Act (HOLC) was essentially a Depression-era footnote—some dusty policy that little changed. The reality is, though, it transformed American homeownership and left a divisive legacy still felt today.

Why Should You Give a 90-Year-Old Law Any Thought?

- If you have ever refinanced a mortgage, you can thank the HOLC or assign guilt.

- If you know of “redlining”—the HOLC contributed to aggravate it.

- Surprising you, if you believe government bailouts are a modern occurrence. First the HOLC accomplished.

This is not only past; this is present as well. This explains why your loan conditions, interest rates, and even the worth of your neighbourhood can currently seem the way they do.

2: What Act Applied to Home Owners Loans? In plain English,

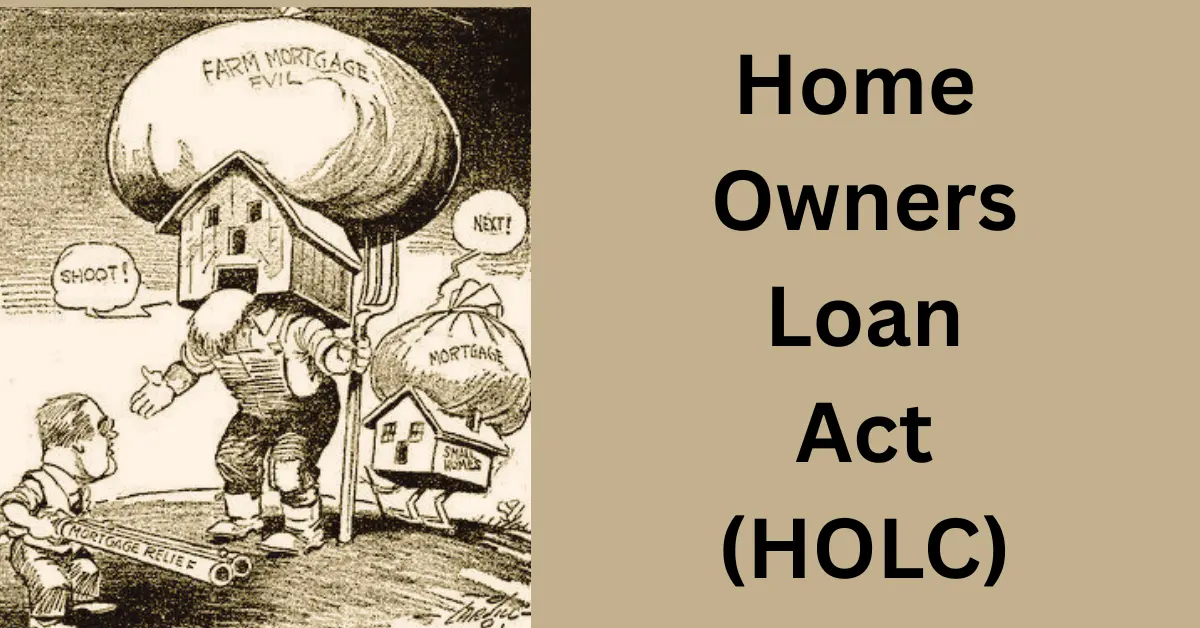

📜 The Fundamentals A Helpline During the Depression

See this: 1933 here is. Banks are failing. One in four homeowners are about to be without their homes. Now let me introduce the Home Owners Loan Act, a government Hail Mary meant to stem the bleeding.

Simple Version of How It Worked

- Saying, “Hey banks, stop foreclosing—we’ll refinance these loans ourselves,” the U.S. government intervened.

- Unlike the conventional 5-10 year loans, homeowners obtained longer terms—15 to 25 years.

- Banks paid (as, to be honest, they usually come first).

Why Was This a Huge Deal?

Previously before the HOLC

- Short-term mortgages, such those for a 5-year sprint to pay off your house

- Not any refinancing choices; miss a payment? Home, bye-bye.

After following the HOLC

- Refinancing became standard —sound familiar, modern homeowners?

- Reduced interest rates, some as low as 5%—cries in 2024 rates

For what replaced the HOLC?

Though its legacy lives on in FHA loans, the HOLC closed in 1951.

VA loans (another New Deal legacy, for veterans).

contemporary bailouts like to those of the 2008 crisis and COVID rescue.

Fascinating fact: The HOLC served as a sort of “test run” for the modern mortgage system.

The Dark Side: ugly roots of redlining

It get messy here. The HOLC produced neighborhood “risk maps” with color codes:

Green indicates “Best” (rich white neighborhoods).

Red indicates “Hazardious” (Black, immigrant areas).

This “redlining” made it almost impossible for minorities to obtain loans, a stain still seen in housing disparity today.

3: 5 Startling Facts About the Home Owners Loan Act (That’s Will Make Your Jaw Drop!)

“The HOLC was just a simple mortgage relief program, right?”

Once again.

Most people believe the Home Owners Loan Act (HOLC) was only a Depression-era well-meaning legislative measure. Benevolent behind the scenes, though It was loaded with debate, legal gaps, and long-term effects still felt by homeowners now.

Let us dissect five startling facts—some terrible, some useful.

🔥 Fact 1: It created modern refinancing. However, with a nasty side effect

Prior to the HOLC:

- There was nothing known as refinancing. Should you find yourself unable of paying? Your house vanished from tough luck.

Following the HOLC

- Thank God; homeowners may at last renegotiate loans.

- Terms ranged from five years to fifteen to twenty-five years, much more reasonable.

The catch is

- The initial “redlining” maps produced by the HOLC graded areas based on income and color.

- “Hazardous” (also known as minority) locations were designated in red, rendering loan almost impossible there.

👉 Funny how a program meant to “help” also prepared the ground for decades of discrimination.

😆 Fact 2: Today You Are Not eligible for a HOLC Loan But His Legacy Lives On

“Can I apply for a HOLC loan in 2024?”

Not that great; it finished in 1951.

Here is what took place instead, though:

- FHA loans, the most well-known cousin of the HOLC.

- VA loans, another spin-off of the New Deal for veterans

- COVID-19 mortgage relief—proof the government still employs HOLC-style bailouts.

Basically, The “refinance and rescue” paradigm of the HOLC just changed; it never actually perished.

😥 Fact 3: It unintentionally contributed to housing discrimination (Big Time).

Redlining was not invented by the HOLC; rather, it was supercharged.

In what sense?

- Its “risk maps” labeled Black/immigrant regions as “high-risk.”

- For decades banks denied loans using these maps.

- As so, Rich differences, segregation, and contemporary “food deserts.”

👉 Amazing how still Starbucks opens today reflects a 1930s policy?

Fact 4: It was a bail-out… For BANKS, Not Just Homeowners

” Wait, the HOLC helped regular people?”

Indeed; but banks received the better bargain.

- The government paid banks defaulting mortgages so they wouldn’t lose money.

- Though they still had to pay, homeowners paid less.

- Not unfamiliar at all. Cough 2008 bailout cough.

👉 Some things never change; banks always triumph.

🔥 Fact 5: Some HOLC Loans had 5% interest (yes, really!).

“5% Interest?” Where am I supposed to sign?

- Some HOLC loans in the 1930s barely registered at 5%.

- That contrasts with the 6–7% rates of today (painful).

Why would that be so low?

- The government sponsored rates to help homeowners survive.

- After inflation? That sounds like a 2% loan right now.

What moral lesson the narrative offers? Travel back to 1933 to get a better mortgage.

4: How Homeowners TODAY Affected by the HOLC

“Yeah, but does this 90-year-old law really matter now?”

More than you could possibly know.

1. One of the long shadows of redlining.

- The racist maps of HOLC define the current lending bias.

- Minority areas STILL get less loans (and higher rates).

2. Refinancing: Greatest Gift from HOLC

- Before Holt’s Congress? Not such a thing as refinancing.

- Just now. For struggling homeowners, it’s a lifeline.

3. protections against foreclosure began here.

- The HOLC confirmed government-backed mortgage relief is effective.

- See: delays in COVID-19 payments, 2008 bailouts. Every current housing rescue strategy includes the DNA of the HOLC.

Read more about: 5 Secrets Your VA Home Loan Payment Calculator Isn’t Telling You (But Should!)

5: HOLC FAQs – Your Burning Questions Answered!

“Right, the Home Owners Loan Act is just ancient history with no bearing today.”

Incorrect once more.

People believe this 90-year-old rule has no bearing on them; nevertheless, if you have ever sought a mortgage, dealt with redlining, or heard about government bailouts? You have seen the fingerprints of the HOLC.

Let’s address the most often asked questions by actual individuals regarding the HOLC—the ones Google searches daily.

1. “Is the Home Owners Loan Act still active?”

Short response: Not true. Officially closing its doors in 1951, the HOLC

The twist is that here is also

- Modern initiatives like FHA loans, VA loans, and even mortgage relief during COVID-era live on in her ideas.

- The model of “refinance and rescue”? That matches 100% HOLC DNA.

👉 You are therefore essentially using a HOLC loan’s grandkids even though you cannot obtain one right now.

2. “Can I have a HOLC loan right now?”

Not so much—but here’s what you CAN do instead:

- Thanks, HOLC inspiration; low down payments and simpler credit standards define FHA loans.

- VA Loans: Zero down payment for another New Deal descendent, veterans.

- Post-2008 crisis assistance via HARP/HAMP programs reflects same “save homeowners” attitude.

Consider these as the contemporary updates for the HOLC.

3. “Did the HOLC bring about redlining?”

Not precisely, but it gave it great boost.

- The HOLC produced color-coded “risk maps,” green = “safe,” red = “hazardous”.

- For decades banks denied loans to Black/immigrant areas using these maps.

- The outcome is Segregation, disparities in wealth, and contemporary lending bias.

The HOLC did not begin redlining… but it gave banks a biassed road map.

4. “What’s the difference between HOLC and FHA?”

HOLC:

- Program for emergency rescue between 1933 and 1951.

- refinanced current mortgages to stop foreclosures.

FHA:

- 1934-created permanent system still in use today.

- Insures loans (therefore banks assume less risk).

HOLC was the “ER,” FHA is the “family doctor.”

6: Final Thought: What Holc Says Today

“Okay, but for ME what’s the lesson?”

glad you enquired. The practical lesson this 90-year-old statute offers is:

📌 1. History Repeats Itself—especially in housing.

- 2008 downturn? HOLC-style bailouts.

- Relief from COVID-19 Payment pauses based on HOLC style.

- Redlining’s legacy Still influencing house values right now.

📌 2. Things stay the same more things change.(Thank the HOLC; refinancing is a superpower.)

- Before 1933, if you couldn pay? You moved out of your residence. Right now. You can delay payments, extend, or renegotiate.

👉 Use this authority sensibly.

📌 3. Stay Woken on Redlining

- Check the HOLC map for your house (search online—it’s eerie yet insightful).

- Support fair lending rules as mistakes made by the HOLC shouldn’t be repeated.

😆 🚀 Last Thought

The HOLC was not only a band-aid for the Depression. It was, all things considered, a blueprint for contemporary homes, with problems.

Your action?

- first-time buyer? Consult FHA loans.

- Having financial difficulties? Look at refinancing (HOLC’s gift to you).

- Just fascinated by history? Explore those maps of redlining more closely.